Did you know your home loan can be worth money?

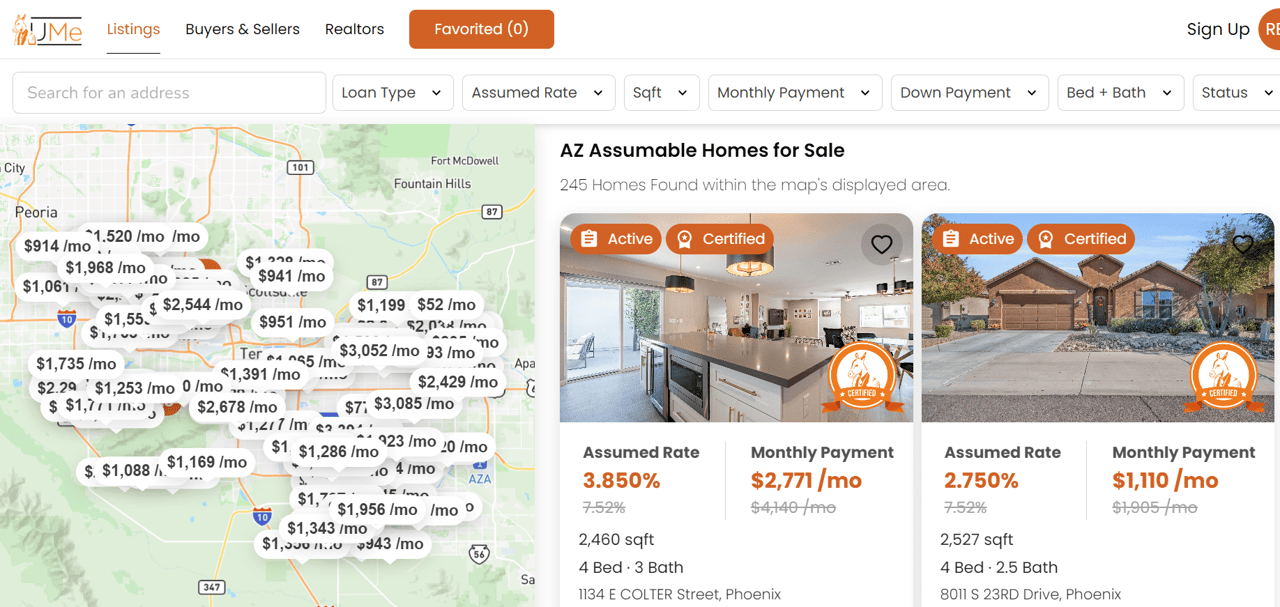

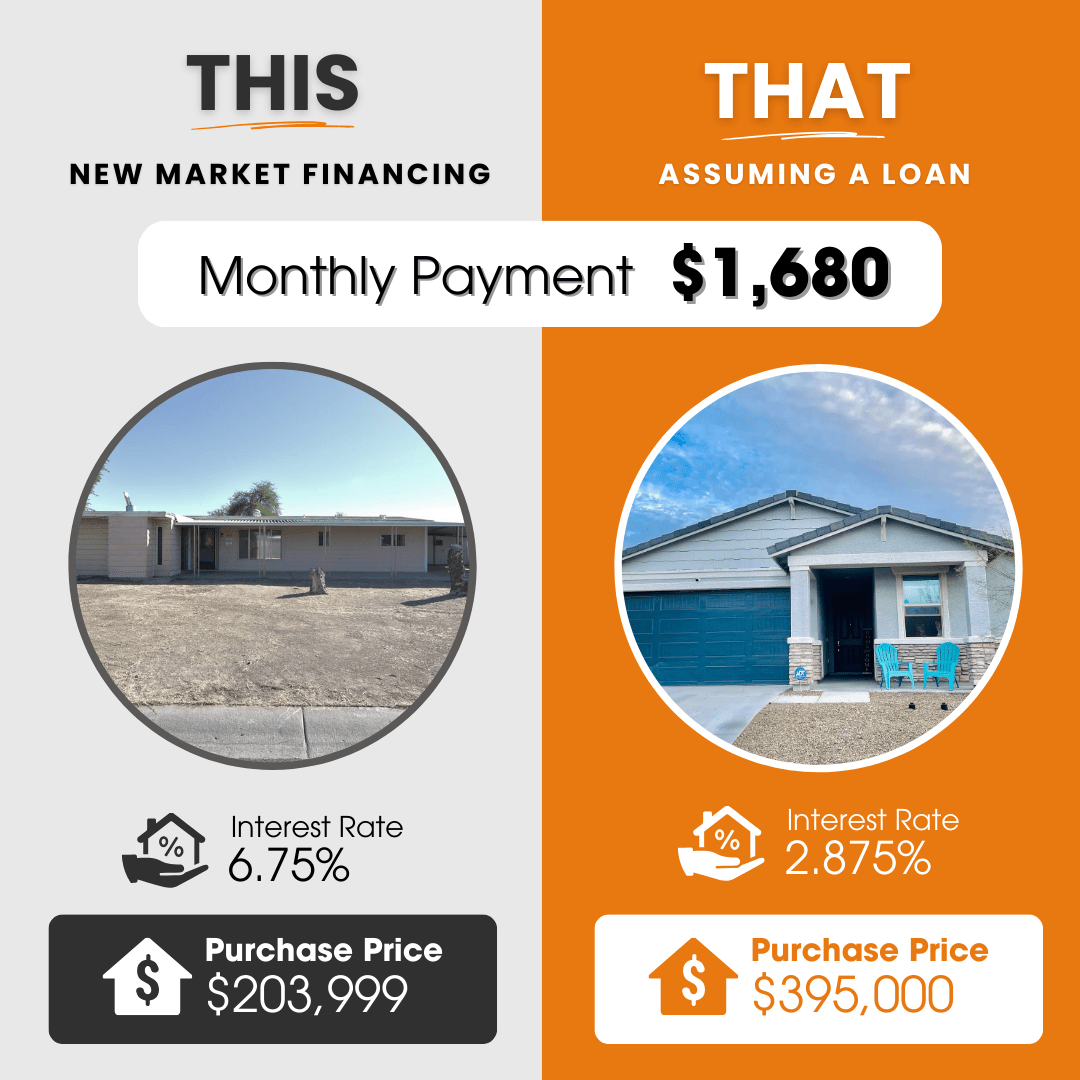

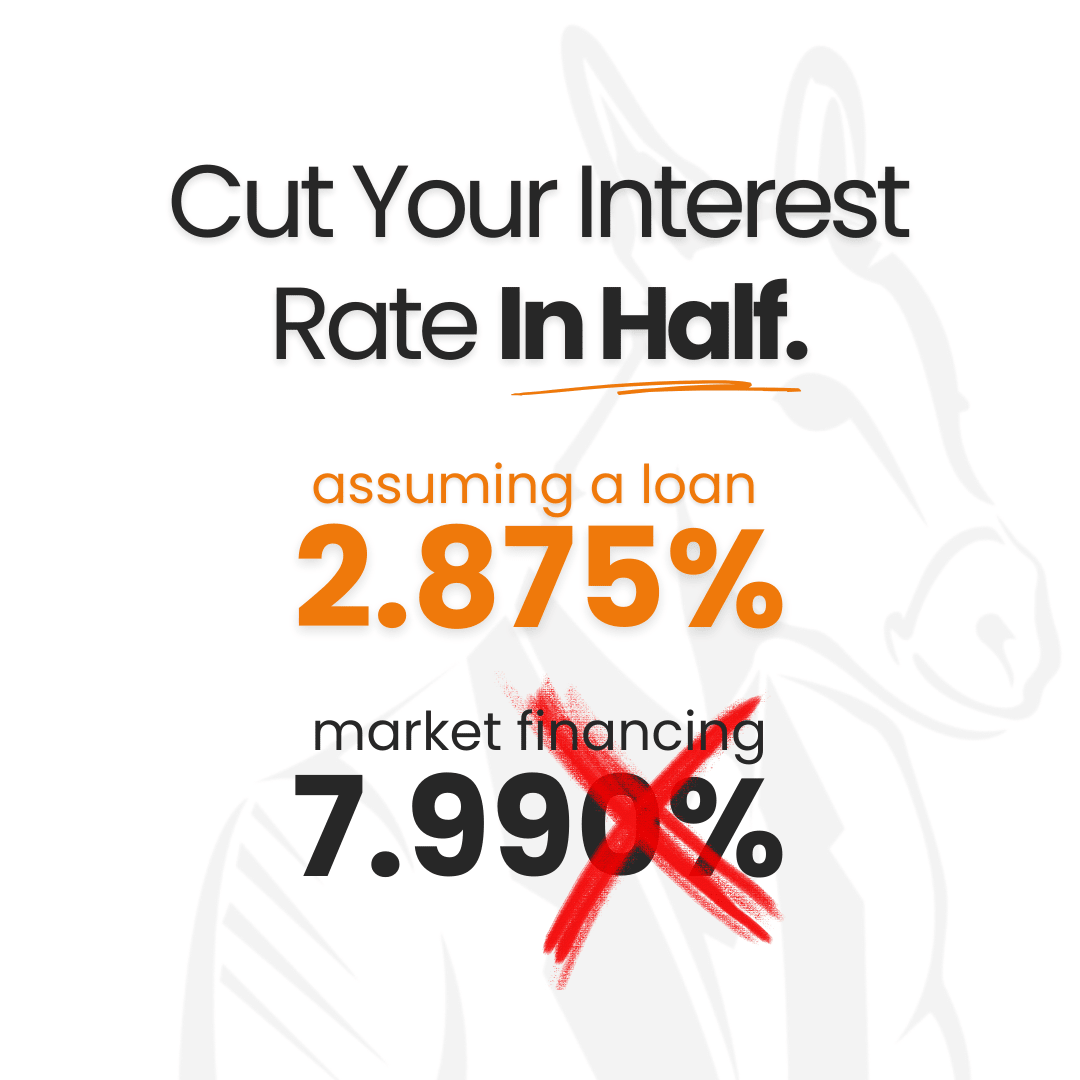

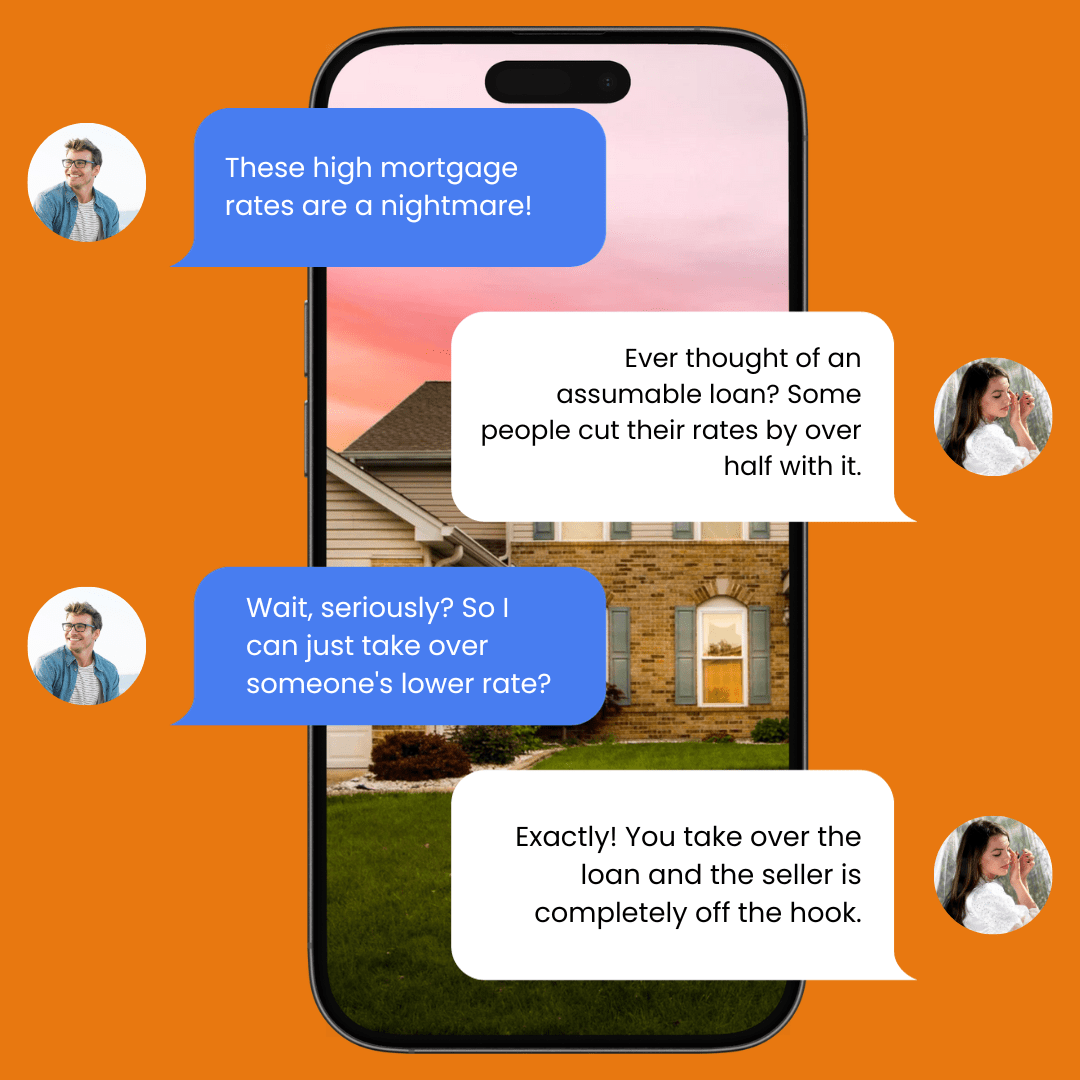

A mortgage assumption, simply put, is taking over another person’s mortgage with all its terms. This would include the remaining length of the loan, the INTEREST RATE AND PAYMENT, as well as the current balance. With the help of the right professionals, you can identify homes for sale that have assumable loans. Many on the market right now carry rates ranging between 2.25% and 5%. To put that in perspective, if you purchase a home with a $500,000 assumable loan with a 3% interest rate, your principal and interest payment would be $2108. Buying the same home with a current market rate of 7.75% would yield a payment of $3582. That’s a savings of over $1400 per month! With approximately 25% of the real estate market having assumable loans, there are more than enough options to choose from.